TABLE of CONTENTS

Introduction

FinCEN’s crypto actions: 2011-2019

2011:MSB definition includes virtual assets

2012: U.S.-servicing MSBs within regulatory scope

2013: CVC-dealing MSBs are money transmitters

2014: Crypto Miners are not MSBs

2015: First Action vs CVC Exchanger-: Ripple Labs

2017: First Action vs Foreign Exchange: BTC-e

2018: CDD Rule for MSBs comes into effect

2019: FinCEN consolidates its crypto regulation

Introduction

The Financial Crimes Enforcement Network (FinCEN) is the United States’ primary Anti-Money-Laundering (AML) and Combating-Funding-of-Terrorism (CFT) regulator.

Since 2011, FinCEN has kept a relatively relaxed approach in dealing with cryptocurrencies (also referred to as virtual assets or virtual currencies by different regulators), preferring to release periodical advisory documents, guidances, and details on enforcement actions it took against money launderers.

This lack of a clear and transparent policy on virtual currencies has created confusion in the crypto industry on how this important regulator defines assets such as Bitcoin and Ethereum.

In 2019, FinCEN finally released a new guidance on convertible virtual currencies (CVCs) and how they apply to various business models, that consolidates nearly a decade of regulatory documentation.

This, coupled with several interviews with the FinCEN director Kenneth Blanco, now provide a crystal-clear view on how the U.S. Treasury’s leading AML/CFT watchdog interprets virtual asset ownership and transmittals.

In this article, we take a look at how FinCEN helped redefine the regulatory landscape for virtual assets over the last decade.

Which crypto-related actions have FinCEN taken since 2011?

July 2011: Final Rule on MSB definition includes virtual assets

In its regulatory update Definitions and Other Regulations Relating to Money Services Businesses, FinCEN changes its definition of money service businesses (MSBs), companies that fall under its regulatory scope, to include virtual currencies through the phrase “other value that substitutes for currency”.

This is important, as, under the requirements of the BSA, MSBs are obligated to keep an AML program and comply with reporting, registration, and data recording requirements.

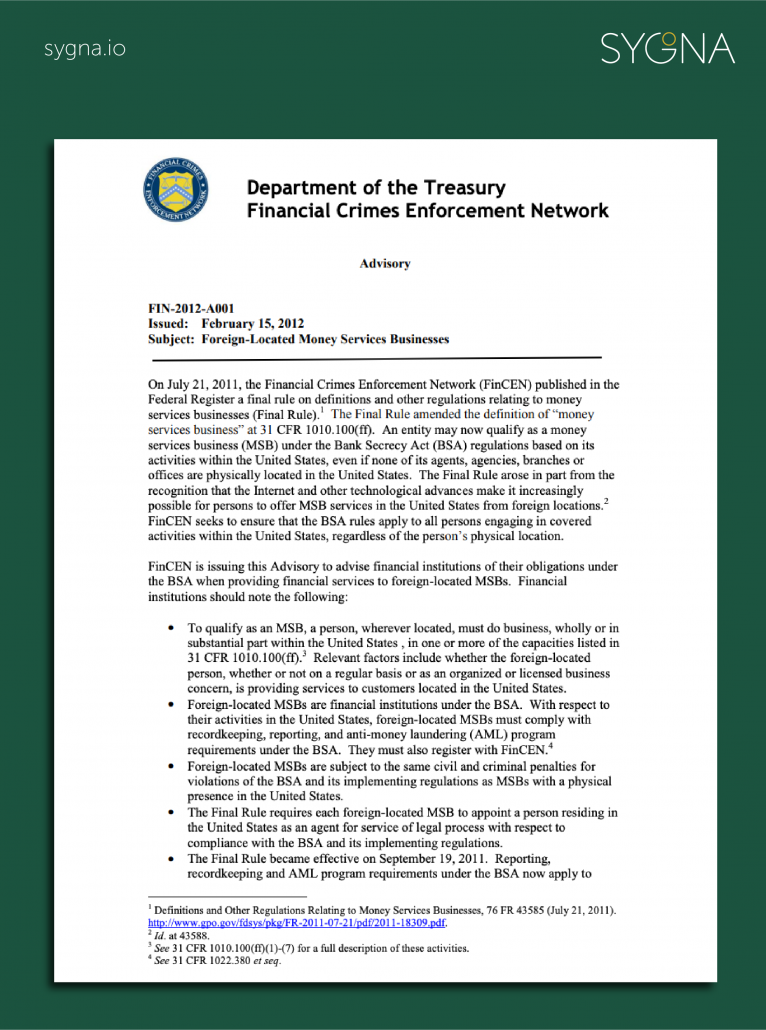

February 2012: MSBs with U.S. customers are under FinCEN’s regulatory scope

In February 2012, a new FinCEN guidance decrees that MSBs who deal with U.S. customers are subject to FinCEN regulations, irrespective of where they are based. This is an important regulation that acts as a deterrent to companies wishing to engage with the lucrative U.S. market without following the correct regulatory procedures. In 2019, FinCEN’s repeated references to this fact, as well as their May guidance, played a large role in leading exchanges like Binance closing up access to their platforms in the States and instead, issuing separate exchanges like Binance U.S. specifically for the world’s biggest cryptocurrency market.

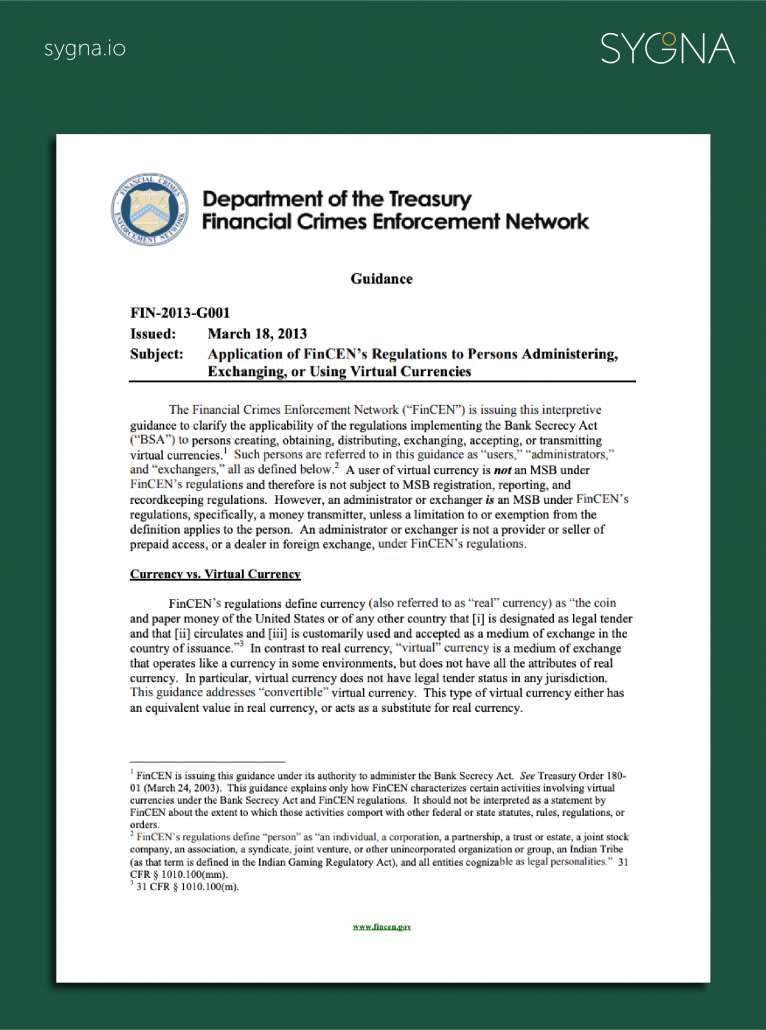

March 2013: MSBs who deal with CVCs are money transmitters

On March 18 2013, in response to growing uncertainty and gray areas on what constitutes an MSB and/or money transmitter, FinCEN issued their guidance Application of FinCEN’s Regulations to Persons Administering, Exchanging, or Using Virtual Currencies, to clarify how persons or businesses involved with “exchanging, accepting and transmitting” virtual currencies should be treated.

Essentially FinCEN declared that virtual currencies are the same as traditional currencies and that MSBs (but not users) who deal with convertible virtual currency (CVC) are defined as money transmitters, and must, therefore, comply with AML/CFT regulations by keeping and reporting transaction records and registering with FinCEN.

FinCEN also defined a Convertible Virtual Currency (CVC) as an unregulated virtual currency that has the ability to act as a replacement for real and legal currency. It has an equivalent value in fiat currency and can be exchanged for real money. The CVC issue has come to the fore with the May 2019 FinCEN guidance.

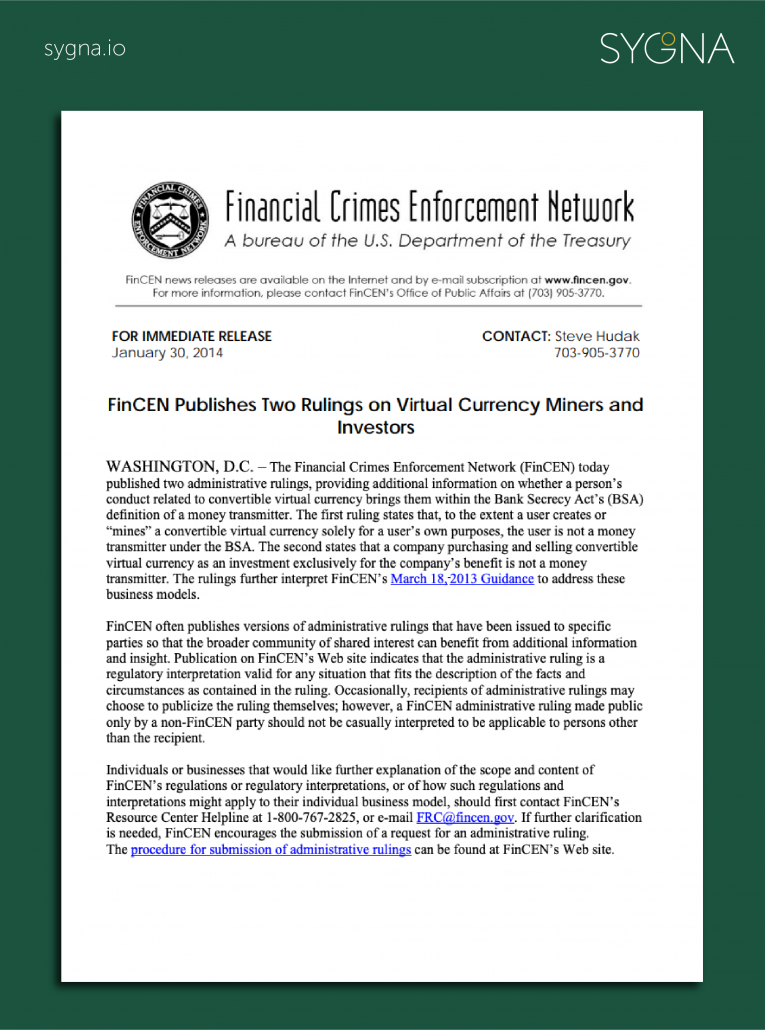

January 2014: Crypto Miners are not Money Service Businesses (MSBs)

In 2014, FinCEN clarified 2013’s guidance by issuing more definitive administrative rulings applicable to virtual assets. Most notably, the Administrative Ruling on the Definition of User in Context of Mining (January 2014) declared that miners who mine virtual assets for personal use or companies that purchase and sell convertible virtual currency (CVC) only as an investment are not MSB’s.

May 2015: First Action vs CVC Exchanger- Ripple Labs fined $700k

After Ripple Labs failed to register as an MSB after launching their XRP virtual currency, a digital token to settle payments(now one of the world’s most popular virtual assets), FinCEN fined Ripple Labs in the first civil enforcement action against a cryptocurrency exchanger. FinCEN fined Ripple $700,000 and accused the crypto company of:

“willfully violating several requirements of the Bank Secrecy Act (BSA) by acting as a money services business (MSB) and selling its virtual currency, known as XRP, without registering with FinCEN, and by failing to implement and maintain an adequate anti-money laundering (AML) program”

Ripple Labs ultimately settled with FinCEN for $450,000, promising to take “enhanced remedial measures” in order to comply with BSA regulations.

July 2017: First Action vs Foreign Exchange- BTC-e fined $110 million

FinCEN takes its first action against a foreign-based MSB by fining the controversial virtual currency exchanges BTC-e, popular with money launderers and cybercriminals at the time, a staggering $110 million for operating without a license and conducting criminal behavior. Russian national Alexander Vinnik was arrested in Greece for willfully violating the US’ global AML laws. The exchange has since shut down.

2018: The Customer Due Diligence (CDD) Rule for MSBs comes into effect

FinCEN reminds financial institutions to adhere to its Customer Due Diligence (CDD) Rule, which was introduced in 2016 and changed existing BSA regulations, as follows:

- Identify and verify a customer’s identity

- Identify and verify the identities of the beneficial owners of companies opening accounts

- Understand the nature and purpose of customer relationships to develop customer risk profiles

- Conduct ongoing monitoring to identify and report suspicious transactions and, on a risk basis, to maintain and update customer information

2019: FinCEN consolidates its crypto regulatory approach

With the U.S.’s presidency of the FATF providing an opportune time to establish a strong and cohesive global framework for the AML/CFT regulation of virtual assets, FinCEN became noticeably more active towards the crypto industry in 2019.

April 2019

FinCEN penalizes an individual for the first time for failing to register as a money service business, in a move that shocks the crypto industry. Eric Powers was fined $35,000 after operating “willfully” as a peer-to-peer (P2P) exchanger of convertible virtual currencies, facilitating over 200 Bitcoin transactions to the value of an estimated $5 million.

FinCEN sent a clear message to the crypto industry with this enforcement of the BSA, showing that all money transmitters were in their crosshairs, irrespective of their size, in a statement by Mr. Blanco that laid out the reasoning behind the agency’s action:

“It should not come as a surprise that we will take enforcement action based on what we have publicly stated since our March 2013 Guidance—that exchangers of convertible virtual currency, such as Mr. Powers, are money transmitters and must register as MSBs. In fact, there were indications that Mr. Powers specifically was aware of these obligations but willfully failed to honor them. Such failures put our financial system and national security at risk and jeopardize the safety and well-being of our people, as well as undercut responsible innovation in the financial services space.”

Ken Blanco, FinCEN director on the Eric Powers case

May 2019

FinCEN consolidates nearly a decade of previous statements on virtual currencies (2011-2019) in a detailed interpretive guidance. FinCEN’s CVC guidance, Regulations to Certain Business Models Involving Convertible Virtual Currencies, warns crypto businesses that they are in fact MSBs due to their transacting with CVCs, and are therefore in breach of the BSA if they don’t register and adhere to FinCEN policies.

FinCEN takes further aim at decentralized applications (dAPPS) and says some of them are in fact also MSBs and therefore under their jurisdiction.

October 2019

FinCEN issues a joint statement with the U.S. Securities and Exchange Commission (SEC) and U.S. Commodity Futures Trading Commission (CFTC) to provide a united AML/CFT front and explain how they view the regulation of digital assets. This was an important precursor to their closer cooperation in 2020, as expounded on by new proposed laws such as the Crypto-Currency Act of 2020 draft.

November 2019

FinCEN declares that stablecoins like Libra are also to be classified as “money transmitters”.

“It does not matter if the stablecoin is backed by a currency, a commodity, or even an algorithm – the rules are the same.. Just because you say you are a banana, doesn’t make you a banana… FinCEN applies the same technology-neutral regulatory framework to any activity that provides the same functionality at the same level or risk, regardless of its label. It is not what you label it, it’s the activity you actually do that counts.”

Ken Blanco on stablecoins like Libra

December 2019

A new bill, dubbed the Cryptocurrency Act of 2020, aiming to allocate responsibility for the allocation of virtual currencies to various federal agencies, has been proposed to the U.S. Congress. The act identifies FinCEN, the SEC and CFTC as the leading digital asset regulators in the federal government and emphasizes their mutual future cooperation.

Conclusion:

In hindsight, it’s now clear that FinCEN in 2019 successfully consolidated its regulatory policies for virtual currencies and laid a foundation for its policies and cooperation with other leading FIUs for 2020 and the new decade. With Mr. Blanco’s latest combative comments showing that FinCEN has no intention of abating its systematic approach to regulating virtual currencies, cryptocurrency industry stakeholders need to verify that they are not subject to FinCEN’s regulations, and if they are, that they understand exactly how FinCEN may impact their business. Failure to do so may have devastating consequences.