It’s time to build trust and credibility in the cryptocurrency industry because of the regulatory environment, not in spite of it, says Elsa Madrolle, CoolBitX MD International.

– 7 November 2020

Just one week after the EU unveiled its monumental Digital Finance Strategy, US CFTC commissioner Dan Berkovitz was in a fireside chat with Solidus Labs at DACOM, explaining his stance on regulation in the crypto space from a US perspective.

“In the US we are fortunate to still be the global leaders in capital formation and derivatives… People come to the US because it’s an honest market… Rules will be enforced. There is trust and credibility because of the regulatory environment”.

Berkovitz then highlighted that the benchmark for the price of Chinese corn is still a Chicago Board of Trade futures index for these reasons and likened the newness of digital assets to the creation of financial futures – a new asset class in its own right, albeit one that merely poses new (but not insurmountable) challenges to regulate.

In 2017, JPMorgan’s Jamie Dimon compared Bitcoin to the 17th century’s tulip frenzy (and quietly proceeded to spend a small fortune to build out his blockchain division, complete with a proprietary coin).

Source: Framingbitcoin.com

Source: Framingbitcoin.com

“It’s worse than tulip bulbs”, Dimon had famously said at a Barclays banking industry conference. “It won’t end well. Someone is going to get killed. Currencies have legal support. It will blow up.”

Regulators and industry around the globe are investing significant resources to provide legal support to digital assets and their infrastructure. In doing so they are predictably prompting widespread discontent from the most liberal within the community, but most importantly, they are validating the asset class on the world stage.

By allocating so many resources in a resource-stretched environment, we are recognizing that digital assets are here to say, that Bitcoin is “a thing”. This comes with the tacit understanding that our current geopolitical environment may desperately need the very solutions that blockchain-based assets can offer as the current pandemic rips through our economies.

On the eve of 2021 the global crypto regulatory scene remains messy and the “sunrise problem” of regulation being established on different schedules in different ways further adds yet more complexity.

The state of crypto regulation

The motivations behind global regulatory efforts of the burgeoning crypto industry can be summarized by four objectives:

- Protection of the individual

- Mitigation of threats to the global financial system

- Promotion of innovation

- Financial inclusion

This is a veritable existential crisis for the industry, stemming from regulation trying to marry these multiple conflicting objectives. If we want to attract liquidity to these markets, thus institutional flow, we have to protect the consumer and this can only come through adequate regulation. However to pursue financial inclusion objectives, innovation cannot be thwarted.

Looking across the world is a patchwork of regulatory disparity for the crypto space.

North America

On October 27, 2020, FinCEN and the Fed published in the Federal Register a joint notice of proposed rulemaking to modify the threshold in the Bank Secrecy Act (BSA) requirement for financial institutions to collect and retain information on funds transfers and transmittals of funds. The proposal would reduce this threshold from $3,000 to $250 for funds transfers that begin or end outside the United States, including for financial institutions.

This proposal effectively pulls banks into the AML “Travel Rule” debate currently affecting virtual asset service providers (VASPs), and if adopted in its current form, could significantly impact the ACH payment transfer system, which is a low-cost, slower system than more onerous wire transfers, commonly used for low-to-medium value transactions such as direct debits or payroll.

Neither candidate in the US election has taken a firm stance on the digital asset industry, so there remains complete uncertainty as to the direction of the next administration. The only certainty is that AML enforcement in the crypto space will accelerate as illustrated by high profile cases in 2020.

In Canada, where nearly 400 crypto businesses have already registered as MSBs, FINTRAC has set out an expected schedule for MSBs as new AML legislation goes live on June 1st, 2021. Despite industry protests of insufficient consultation, the timelines set out by FINTRAC are pressing and ambitious.

Europe

The European Union has now drawn a line in the sand and published a monumental proposal for crypto regulation, in an effort to balance support for innovation and consumer protection to entities that wish to conduct business in the EU.

There is a risk that the proposed legislation could favor traditional financial institutions that have already swallowed the pain of earlier EU regulation such as MiFiD (thus will not need to jump further hurdles) over start-ups, on the one hand promoting innovation for the incumbents, on the other stifling it for start-ups who may not survive the financial burden of new compliance.

The network effect is strong in Europe and a cynic might remark that EU officials are more likely to be the alma mater of graying heads of European banking than young nomadic digital entrepreneurs.

Either way, the impact on DeFi could be so unforgiving that start-ups may choose to exit the EU altogether, which is not the desired outcome. MiCA doesn’t even cover AML/CFT directly, so the European AML Directive still needs to be amended to better align with the Financial Action Task Force (FATF) guidelines. In a surprising move, the UK in October 2020 took a firm stance on crypto derivatives, banning them from retail investors, unlike traditional derivatives. Ongoing Brexit uncertainties further complicate the European landscape given the size of the UK in the regional financial markets.

Asia

The landscape in Asia is more promising. Regulators are unveiling their plans, with countries like Singapore setting the tone, issuing consultations and requesting public feedback but firmly aligning itself with FATF AML guidelines.

China is making increasing noises about its digital currency while Japan, with its powerful SRO, Korea, Hong Kong and others are creating or amending various laws to better regulate crypto-asset service providers, as they too work towards full alignment with FATF guidelines.

As the Hong Kong SFC remarked in a keynote speech at Hong Kong Fintech Week, it is their obligation as a FATF member to comply with the guidelines. However, the fragmentation of the region underpins the sunrise issue with some countries still months away from issuing new rules or guidance and others implementing nuances such as real-name bank accounts in South Korea.

Other Jurisdictions

Africa and Latin America remain the regions with the most pressing and promising use cases for the emerging asset class but regulation lags behind as governments attempt to organize largely reactive digital strategies, likely watching what happens in the rest of the world first, with a few exceptions. Elsewhere, Australia already has robust crypto regulations in place dating back to 2017.

Meanwhile, the Financial Action Task Force (FATF) is mulling over further guidance, from peer-to-peer transactions to stablecoins, with no stone being left unturned. FATF guidance affects 200+ countries, so the resulting landscape is chaotic as regulators strive against the clock to align with guidance that sometimes conflicts with their original stance.

At the crossroads of crypto regulation

Complicating the regulatory landscape are waves of investigations and high-profile resignations across the industry as scandals and regulators start to shake the ethos of the crypto industry to its core.

The message is clear: As the industry grows up and is validated by regulators paying attention, its participants and leaders will have to as well.

Against the backdrop of a pandemic that has revolutionized human interaction and workplaces, the digital asset industry is at a crossroad in its evolution.

Decentralized digital finance does not have to translate to unregulated finance. With a simplified but effective regulatory framework, digital assets and their service providers can achieve what all agree are common objectives; greater liquidity, greater inclusion, and a better financial system.

In some of the best examples of progressive regulatory innovation, we see sandboxes, trade associations, and extensive consultations resulting in new regulation that is fit for purpose rather than attempts at squeezing new asset-types into old frameworks.

Technology also has the power to alleviate the burden of compliance; FATF President Markus Pleyer highlighted digital transformation as one of his presidential priorities in the FATF virtual asset contact group meeting on Oct 28th 2020.

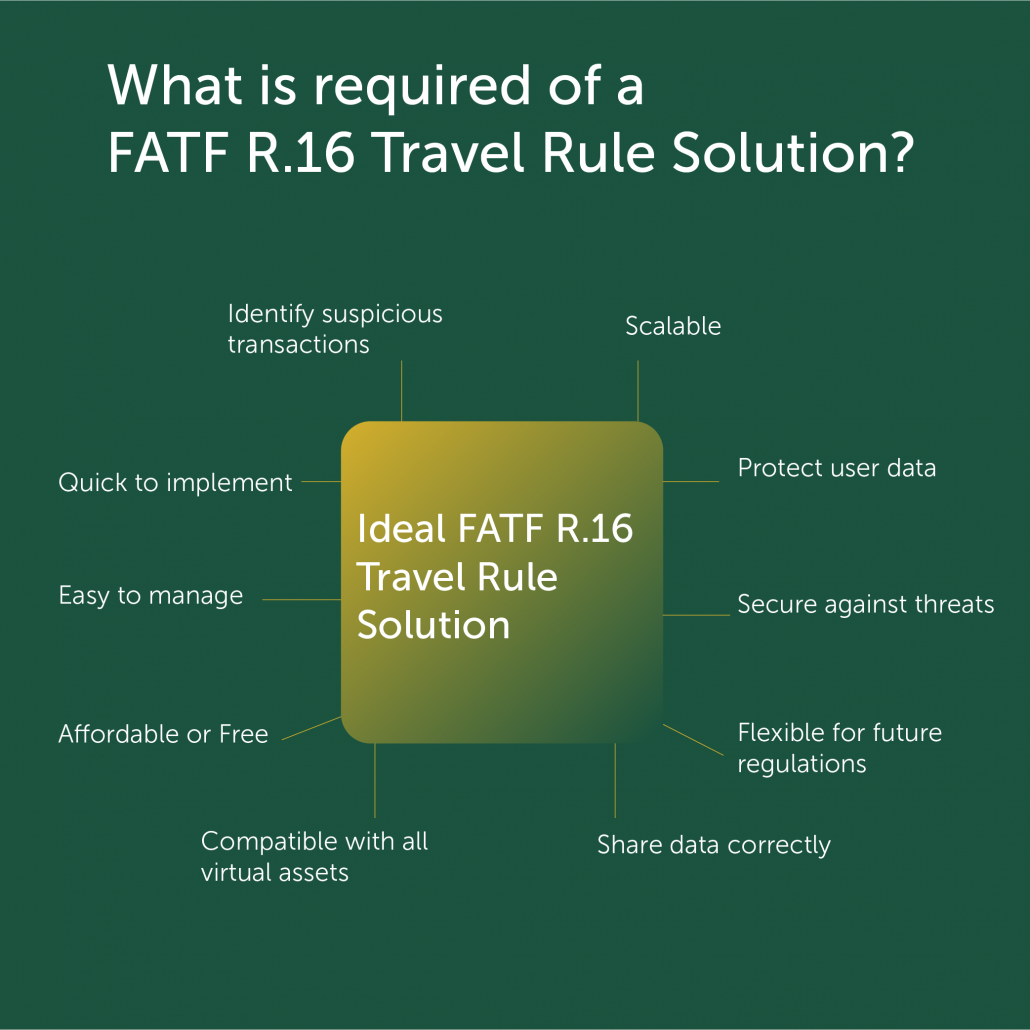

So what’s next for VASPs as they await a global regulatory tsunami?

VASPs can start to prepare today for what they know is on the way; the need for a mandatory regulatory strategy that will have multiple components. FATF guidance is for regulators around the world to issue laws that at a minimum cover VASPs and ensure they:

- Become licensed / registered

- Understand their ML/TF risks

- Have an AML/CFT program

- Conduct customer due diligence

- Keep records

- Report suspicious transactions

- Comply with the ‘Travel Rule’

Some of these initiatives will require mobilizing significant resources to perform due diligence on alternatives, especially against a backdrop of digital transformation so the earlier project teams are set up, the faster VASPs can continue their activities while minimizing the impact on the client experience.

Sygna Bridge and the Travel Rule

We at CoolBitX respect and believe, as a young industry, that we have much to learn from the graying heads of banking. However, this can only be achieved through being creative and open-minded to collaboration.

Sygna Bridge studied the challenges posed by the need to create a Travel Rule-abiding technology. We made the decision not to reinvent the wheel but rather adopt already-tested, familiar systems when they worked well, but also enhance them, where needed, to bring them into the digital asset age and make them suitable to industry-grade security requirements. This followed the model that we had already applied to our hardware wallet solution CoolWallet S. Our wallet blended cutting edge security and technology with a familiar, credit-card shaped format that users could identify with.

Some of our Sygna Bridge decisions below serve as examples of where technical service providers can successfully bridge the gap between proven technologies or formats and innovation. And these decisions were made in consultation with our advisors, institutional investors, and clients.

Why Sygna Bridge is off-chain

We decided to take our solution for the Travel Tule off the blockchain. We have always abided by one of the most important mantras of our industry – just because something can go on blockchain, doesn’t necessarily mean it belongs there.

This is a key tenet often forgotten; too many projects fail due to a misunderstanding of industry dynamics and what blockchain can or cannot solve for, without conducting a thorough analysis of whether it is the optimal technology to solve an existing business problem.

Privacy is a major concern in the exchange of personal information, and offchain technology allows for enhanced privacy and security whilst removing the complication of multiple protocol formats of different currencies. This allows Sygna Bridge to support virtually all assets.

Digital age encryption

Sygna Bridge also uses Bitcoin wallet-type encryption to generate public and private keys that are used to access the network, leveraging the Elliptic Curve Integrated Encryption Scheme (ECIES). This ensures that the technology we use around privacy is suited to the digital nature of transactions we process.

Ease of integration

Being off blockchain and API-based, Sygna Bridge is a centralized network, easy to integrate and familiar to developer teams of any origin and sophistication, using widely-accepted HTTPS protocol encryption. This also greatly facilitates how we propose to approach interoperability through the potential creation of a gateway.

Decentralized data storage and security

We use AWS (Amazon Web Service) which allows us to effectively decentralize the data that we are handling since AWS servers are distributed.

AWS is a state-of-the-art platform that supports the largest online sites in the world and has been certified by multiple ISO certifications (ISO 27001 and ISO 27017) giving Sygna members the assurance of our reliance on a global leader in that field. Additionally, Sygna Bridge itself is also undergoing the implementation of the ISO 27001.

We believe that in order to continue to grow, our industry has to find new ways to give regulators what they want when they need it, offering them transparency, security and reliability in crypto. However, we also do not want to disrupt the user experience and above all we want this industry to thrive because we believe, staunchly, that digital assets are the way of the future.

It is becoming increasingly difficult to find places in Europe that still accept cash, requesting contactless wherever possible. Halloween trick-or-treaters in America are being given virtual currency cards. Street food vendors in Cambodia are accepting bitcoin. And the biggest threat to central banks right now has an unexpected name… Facebook.

The crypto industry needs to hurry up and get over its existential crisis. We will be playing with the big boys (and girls) and we will have to play by their rules, but hopefully, we can also work to help to create new rules.

We have the opportunity now to build upon CFTC Commissioner Berkovitz’s astute remarks by creating and collectively supporting regulatory solutions that add transparency to the whole crypto industry and foster much-needed interoperability and cohesion.

Let’s make sure there is trust and credibility in crypto because of the regulatory environment, not in spite of it. Because we are already there.

Written by Elsa Madrolle

CoolBitX Managing Director, International

To learn more about Sygna Bridge or to set up a meeting with Elsa and CoolBitX’s compliance team, please contact us at services@sygna.io.

Disclaimer: CoolBitX provides these blog posts for general educational purposes only. Information on this blog expresses the opinion of the author only, does not constitute professional legal or financial advice and should not be considered as such.

The author or company may update the information on this article at any time without prior notice and do not guarantee the work to be up to date and accurate. To the best of our knowledge, the information provided here is factual at the time of writing.