Table of Contents:

- Introduction

- Why did FinCEN extend comments to 60 days?

- What is FinCEN’s new private wallet rule proposal?

- What private wallet information must financial institutions record?

- Why FinCEN proposed the new non-custodial wallet rule

- Is the FinCEN NPRM fair and responsible?

- Will Janet Yellen’s Treasury push through the unhosted wallet proposal?

- OCC still flies crypto flag

- Conclusion

- History of FinCEN crypto regulations

(This article has been updated on 3 February 2021 to reflect the January 26th FinCEN extension)

Introduction

The U.S. Treasury and its federal regulator the Financial Crimes Enforcement Network (FinCEN) have again extended the feedback period on a controversial proposal published last year that aims to force companies to track cryptocurrency transactions to and from unhosted (private) wallets by collecting Know-Your-Customer (KYC) information in order to comply with domestic anti-money laundering (AML) regulations.

In December 2020, FinCEN released the Notice on Proposed Rulemaking (NPRM) to help “close the gap” between how financial institutions report big cash and crypto transactions.

Upon its initial release, the crypto industry heavily criticized the proposal and derided it as a last-gasp “midnight rulemaking” effort rushed out by the Trump administration and specifically former U.S. Secretary of the Treasury, Mr. Steven Mnuchin, a vocal crypto critic.

In addition to the new comment period, the FinCEN notice also identifies more statutory authority for the rule under its Anti-Money Laundering Act of 2020 and expands information on the reporting form.

What is FinCEN’s crypto private wallet rule proposal?

FinCEN’s proposed new private wallet AML rule requires custodial crypto accounts, such as banks and money service businesses (MSB) to verify, collect and privately store records of all crypto transactions over $3,000 (or a series exceeding $10,000) involving non-custodial, private wallets that don’t belong to any financial institutions,which FinCEN calls “unhosted wallets”. All transactions above $10,000 need to be reported to FinCEN directly as per the requirements of the Bank Secrecy Act.

This information won’t not be shared to the public domain but should be made available to law enforcement if requested.

In more detail:

Firstly, FinCENplans to mandate cryptocurrency exchanges to collect personal information, including names and addresses of the customers who transfer an aggregate of $3,000 or more per day. This information need not be reported to the financial authority, except under subpoena.

Secondly, the proposal also requires exchanges to file a report whenever a user transfers over $10,000 per day with any “unhosted wallet”; that is, a “ written record or software program” via which a user can store the private keys of the account. Businesses also must report transactions occurring in jurisdictions blacklisted by the U.S., which include North Korea, Iran, and Burma.

The new rule complements FinCEN’s so-called BSA “Travel Rule”, which requires crypto MSBs to exchange user data with transmittal counterparties. The information exchange requirement was introduced by the Financial Action Task Force’s Marshall Billingslea during his U.S. FATF presidency in 2018/2019 and officially adopted in the updated Recommendation 16 during its June 2019 plenary. It is now commonly referred to as the FATF Travel Rule.

Why did FinCEN extend the comments period to 60 days?

On 26 January 2021, FinCEN published an announcement on its website that it would be extending the period for comments to 60 days from the date of its announcement.

According to FinCEN Deputy Director Michael Mosier, the network realized the rule’s 15-day comment period was not enough and that the public needed and demanded more time. It therefore initially added another 15 to 45 days.

“It’s a proposal, it’s not all or nothing. Tell us about what works”

Michael Mosier on FinCEN private wallet rule

Once the Biden administration took over, FinCEN again pivoted, now extending it to 60 days to give industry members, who sent in thousands of comments in the first 15 days, more time to evaluate and provide feedback.

FinCEN is providing the following new 60-day allocation for comments on its December 2020 Notice on Proposed Rule Making on self-hosted wallets for comments on:

- proposed reporting requirements for information on CVC or LTDA transactions over $10,000, or aggregating to greater than $10,000, that involve unhosted (also known as self-hosted or non-custodial wallets) wallets or wallets hosted in jurisdictions identified by FinCEN.

- proposed requirements that banks and MSBs report certain information regarding counterparties to transactions by their hosted wallet customers, and on the proposed recordkeeping requirements.

Timeline of FinCEN’s private wallet rule proposal and extensions

- On 23 December 2020, FinCEN issued the controversial new Notice on Proposed Rulemaking (NPRM) for certain transactions involving convertible virtual currency (CVC) or digital assets with legal tender status (LDTA) forfor cryptocurrency transactions with initially only a 15-day comment window.

- Treasury bowed to public and internal pressure and reopened comments on the proposed rulemaking (NPRM) on 14 January 2021 for an additional 45 days, after receiving and reviewing 7,500 comments submitted during the initial NPRM term.

- FinCEN announces the new 60-day period on 26 January 2021.

What”unhosted” private wallet information must exchanges collect and share?

FinCEN’s proposal requests that companies submit the following information to them:

- Name and address of the customer.

- Type of LTDA (legal tender digital assets) and CVC (convertible virtual currencies) used in the transaction along with the amount and time of the transaction.

- The assessed value of the transaction in U.S. dollars.

- Name and address of each counterparty involved in the transaction.

- Additional information on the counterparty prescribed as mandatory by the Secretary subject to § 1010.316.

- Any form submitted by the customer related to the transaction.

Why has FinCEN proposed new crypto rulemaking?

Former Treasury Secretary Mnuchin said in a December 18 press release last year that the proposal “aims to close the gaps that malign actors seek to exploit in the recordkeeping and reporting regime” and is intended to “protect national security, assist law enforcement, and increase transparency while minimizing impact on responsible innovation.”

Mr. Mosier added that the proposed non-custodial wallet rule will help Treasury distinguish between cash and crypto transactions, close the gap between the $3,000 and $10,000 transaction disclosure requirements, and to help FinCEN “apply the old guardrails where applicable and develop new safeguards for new technology.

By introducing the bill, FinCEN is also trying to effect a wave of disruptive changes it feels is necessary to combat the unbridled growth of blockchain and crypto technology, network scaling, P2P activity between unhosted wallets, privacy coins and coin mixing technology used to obfuscate transactional information associated with Bitcoin and anonymity coins like Monero, ZCash, Dash and beam. These factors are making blockchain analysis increasingly difficult and less effective, which in turn leads to less efficient AML/CFT results.

Is the proposed rule on self-hosted wallets fair?

To assess the fairness of the proposed NPRM, it’s imperative to know what’s at stake. Today, one of the biggest AML accusations leveled against cryptocurrency exchanges is that they don’t know the identities of of non-custodial wallet owners who they transact with. These owners are exchanging, receiving, and sending cryptocurrencies on an exchange’s platform without revealing their ID.

FinCEN wants to change this by proposing regulations that make it mandatory for cryptocurrency exchanges to start collecting their users’ data. This will almost certainly put an end to the seamless transfers and add unwelcome complexity to transmittals for exchanges who are already burdened by strict KYC and Travel Rule obligations . However, similar rules have been applied to banks and financial institutions for years.

Fintech giants like PayPal and Western Union have been abiding by the $3000 recordkeeping rule since 1996. Now, even the crypto industry will adhere to the rules applied to other forms of money transmitters.

Industry reaction

FinCEN usually gives a 30 days period to give a response, however; this particular crypto wallet rule was issued with only 15 days for public comments. The given period ended on 4th January, with over 7.37k comments from the community. Most of the comments talk about privacy, and how FinCEN has historically given short shrift to privacy concerns.

The beta document also received negative comments from major FinTech firms like crypto proponent Jack Dorsey’s Square Inc (read their letter here) and big cryptocurrency exchanges like Coinbase, as well as industry associations such as the Chambers of Digital Commerce. They have requested FinCEN to first engage with the crypto industry before applying any AML/KYC rules on counterparties.

In an unfiltered blog post, Elliptic, a leading blockchain analysis firm, said they “don’t believe this bill supports the goal of introducing AML/CFT regulations to increase the adoption of cryptos”.

They also shared that “the requirements may actually have the opposite effect, potentially increasing the likelihood of financial crime in crypto by forcing businesses to divert valuable compliance resources where they will have relatively little effect”.

How could FinCEN’s unhosted wallet regulation impact crypto?

The crypto industry has been divided on the possible impact of the self-hosted wallet regulation, with some like BlockTower Capital co-founder Ari Paul saying it will have a “minimal impact” and could have been much worse as no reference was made to transactions between two self-hosted wallets, only those that involve an MSB like a crypto exchange.

“Users effectively already had to KYC withdrawals to unhosted [wallets] in the sense that you have to KYC yourself to get an account with an institution. This just means an added step of validating the withdrawal address.”

Others, like Republican representatives Warren Davidson, Tom Emmer, Ted Budd and Scott Perry appealed to Mnuchin to let Treasury consult with the U.S. Congress first in order to balance law enforcement needs with individual rights and technological innovation.

David pulled no punches in a further statement:

“Over-regulating self-hosted wallets will crush a nascent industry and leave the Unites States behind the rest of the world when it comes to harnessing the power of blockchain and cryptocurrency.”

Here follows some specific challenges that the crypto industry would have to contend with if the proposal became law.

Technical challenges

- Implementing this rule would be technically difficult for exchanges because they would have to force their users to manually enter the required information during the transaction.

- Charities that accept digital assets might not be able to do so since they can’t control who sends them funds in cryptos.

- Exchanges don’t have a built-in mechanism to do the compliance, which is an extra cost to the business. Small and newer exchanges will be greatly affected.

Privacy and anonymity

- The rule, if applied, would reveal the personal identities of private crypto wallets in the case of large transactions.

- Privacy proponents are calling these rules a violation of civil liberties. In addition to the transaction details like name and amount, exchanges will also need to record the physical address of the users.

- Since cryptocurrencies keep a public log of transactions made by a wallet’s address, the government can identify any individual using just one logged transfer made to an unhosted wallet.

Will Janet Yellen adopt FinCEN’s unhosted wallet proposal?

As the Trump administration reluctantly made way for the Joe Biden era on 20 January, industry sentiments were predominantly that Biden appointee and likely new head of the Treasury Janet Yellen will not take such a hardline against crypto as her predecessor.

Yellen, as some might recall, was testifying in front of Congress way back in July 2017 when an attendee quite presciently flashed a “Buy Bitcoin” sign behind her for the cameras. The former Federal Reserve chair has previously mentioned that she thinks blockchain technology is important.

Yet Yellen is certainly no crypto convert if past statements are anything to go by. This year she made both pro-crypto and anti-crypto comments. In October 2018 she said the following:

“I will just say outright I am not a fan, and let me tell you why. I know there are hundreds of cryptocurrencies and maybe something is coming down the line that is more appealing but I think first of all, very few transactions [that] are actually handled by bitcoin, and many of those do take place on bitcoin are illegal, illicit transactions.”

The digital asset sector’s record growth viewed against a weakening U.S. dollar that seems to be losing its hegemony on world markets after nearly a century of dominance will put Yellen and others in the Biden administration under tremendous pressure to keep crypto in check.

In fact, many of the industry’s regulatory think thanks and blockchain associations believe that the new proposal, despite the comment extension, is already a fait accompli, and that once it is incorporated into U.S. law, others like the FATF will soon follow with their own versions.

In fact, there are even rumors circulating that the comment extension is not really a courtesy to the crypto industry as much as a well-disguised opportunity for FinCEN to connect with the FATF during its February 22 plenary and align their private wallet regulation strategies.

OCC still flies crypto flag

While FinCEN has proposed an aggressive reporting rule and the SEC and CFTC respectively took action against Ripple and BitMEX last year, the Office of the Comptroller of the Currency (OCC) and its outgoing head Brian Brooks have been lauded for their forward-thinking reforms that aim to leverage the cryptocurrency industry to improve and innovate the U.S. banking systems.

On the same day as a comment period for the proposed FinCEN’s rulemaking, OCC announced that the banks can use stablecoins to conduct payments and other activities and that financial institutions can participate in blockchain networks.

Unfortunately, Brooks has stepped down as Acting Comptroller this week, the latest in a list of casualties as Biden takes over.

Conclusion

With the cryptocurrency sector’s market cap finally crossing $1 trillion in recent weeks, any regulatory criticisms are making the industry jittery, as it may recall how a series of legislative and regulatory crypto actions and bans by countries did much to derail the last bull run.

Certainly, if European Central Bank president Christine Lagarde’s recent comments, where she called for global AML regulations to curtail Bitcoin’s “funny business” are anything to go by, the virtual asset industry can prepare itself for another tumultuous ride in 2021. The only difference is this year the stakes are bigger than ever.

History of FinCEN’s crypto regulations

Here follows some of FinCEN’s cryptocurrency regulations over the last decade:

- July 2011: FinCEN changed its definition of MSBs by including virtual currencies under its regulatory scope.

- February 2012: MSBs that have customers from the U.S. were included under FinCEN’s jurisdiction.

- March 2013: FinCEN issued guidelines clarifying how to treat individuals and businesses involved with virtual currencies.

- January 2014: Crypto miners were excluded as MSBs.

- June 2020: Financial Action Task Force (FATF) issued guidance for virtual currencies and virtual currency providers to abide by the Travel Rule in the same manner as banks and other financial service providers.

- December 2020: Announced the Notice of Proposed Rulemaking (NPRM) on unhosted wallets.

Written by Werner Vermaak,

Sygna Editor

Disclaimer: CoolBitX provides these blog posts for general educational purposes only. Information on this blog expresses the opinion of the author only. It does not constitute professional legal or financial advice and should not be considered as such. The author or company may update the information on this article at any time without prior notice and do not guarantee the work to be up to date and accurate. To the best of our knowledge, the information provided here is factual at the time of writing.

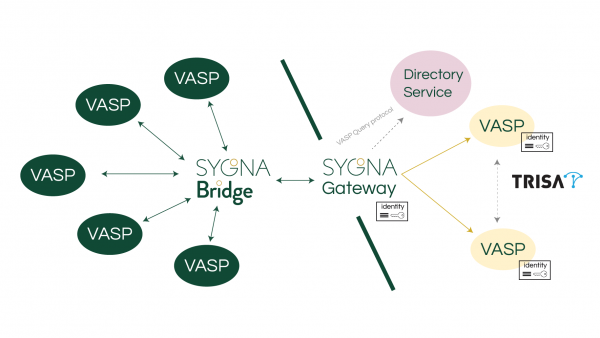

About Sygna Bridge

Sygna Bridge is a simple FATF Travel Rule API messaging network solution developed by CoolBitX to help VASPs share compliance-required transaction information with counterparts securely and with flexible privacy.

In September 2020 CoolBitX conducted the first interoperability proof of concept with CipherTrace’s TRISA solution using the IVMS101 messaging standard.

With over 25 MoUs signed with VASPs on 5 continents, and a strategic partner in blockchain analytics pioneer Elliptic, Sygna Bridge is the right choice to help your crypto-asset service provider comply with the FATF’s Travel Rule and other AML regulations to you get licensed in jurisdictions worldwide.

To learn more or request a demo, please contact services@sygna.io.